In line with the nation’s digital transformation initiatives, the Central Bank of Malaysia (“BNM”) has on 4th January 2022 issued a discussion paper (“Discussion Paper”) on its proposed Licensing Framework for Digital Insurers and Takaful Operators (“DITOs”). As there is ample space for innovation of insurance and takaful business in Malaysia, the issuance of this Discussion Paper is a most welcome step by BNM to regulate and guide the emergence of DITOs in the country.

The objective of the Discussion Paper is to address protection gaps in Malaysia by serving the “unserved and underserved market”, introducing more innovative solutions to cater to diverse protection needs and “enhancing customer experience, wholly or almost wholly through digital or electronic means”.

We highlight below key elements of the Discussion Paper:

1) What is a DITO?

DITO refers to a person licensed under section 10 of the Financial Services Act 2013 (“FSA”) or the Islamic Financial Services Act 2013 (“IFSA”) to carry on:

- digital insurance business; or

- digital takaful business.

The requirement for DITOs to be licensed only applies to digital players who carry on insurance or takaful business (intermediaries such as enablers and managing general agents are excluded from licensing).

Note: While existing licensed insurers and takaful operators are not required to obtain a separate licence under the framework to digitalise their current business operations, an application can be submitted though a separate entity (e.g. a subsidiary or a joint venture company).

2) What then is “Digital Insurance Business” and “Digital Takaful Business”?

Insurance Business

- Under section 5(4) of the FSA, the activity of effecting a contract of insurance or carrying out a contract of insurance* by way of business constitutes carrying on insurance business (“Insurance Business”).

“Digital Insurance Business” on the other hand refers to Insurance Business which is carried on wholly or almost wholly through digital or electronic means.

Takaful Business

- Under section 2(1) of the IFSA, takaful business means the business relating to the administration, management and operation of a takaful fund for its takaful participants which may involve elements of investment and savings and includes retakaful business and a reference to carrying on takaful business may include all or any of the activities set out in paragraph 5(4)(a) of the IFSA (“Takaful Business”).

“Digital Takaful Business” on the other hand refers to Takaful Business which is carried on wholly or almost wholly through digital or electronic means.

Note: Please see section 5(4) of the FSA for details on the activities deemed to be “effecting” or “carrying out” a contract of insurance and section 5(4)(a) of the IFSA for the activities deemed to be “carrying out takaful business” by way of business.

3) DITOs to Operate Wholly or Almost Wholly Through Digital Means

Under the Discussion Paper, while DITOs are expected to utilise digital means for all critical functions including onboarding, underwriting, distribution, policy servicing and claims processing and payment, they are still required to establish a registered office in Malaysia which may only be used for the following limited purposes:

- to allow BNM to communicate with the licensed DITO;

- for administrative purposes;

- to facilitate face-to-face customer complaints; and

- for an investigation by BNM or any other authority.

4) Entry Requirements

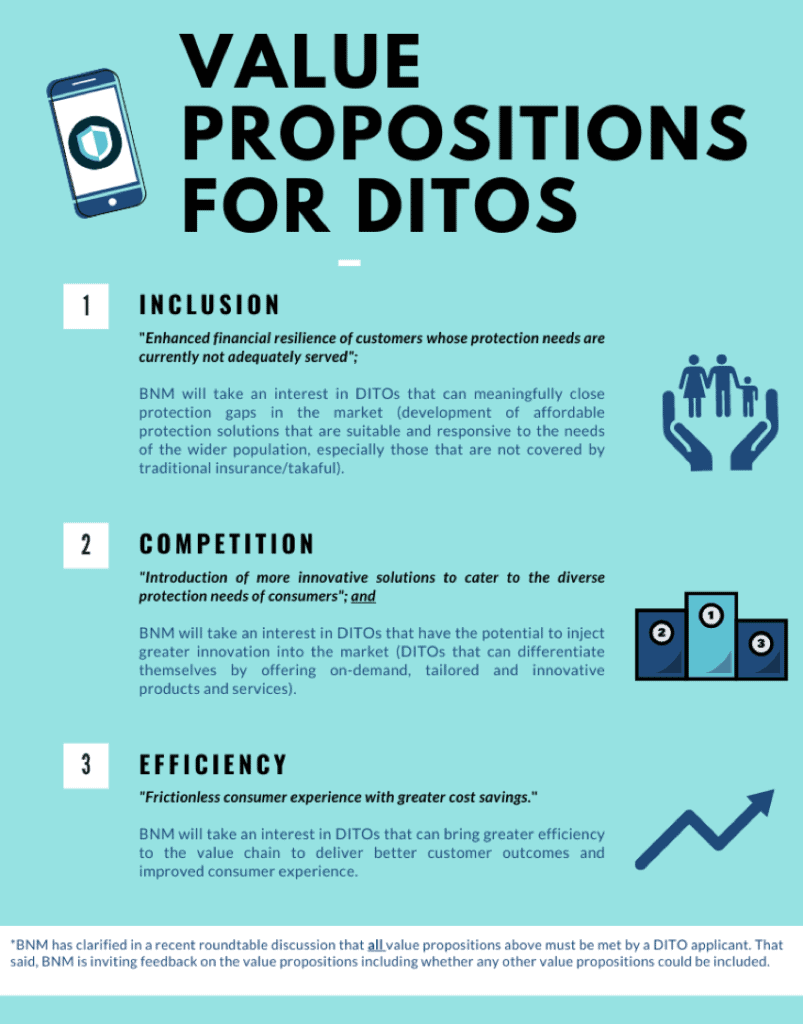

Value Propositions

In line with BNM’s assessment under Schedule 5 of the FSA and IFSA on whether an application will be in the best interest of Malaysia, the Discussion Paper makes it clear that all DITO applicants must demonstrate a commitment in driving value propositions in 3 areas, namely “inclusion”, “competition” and “efficiency”.

Enforceable undertaking by shareholders

Shareholders of a DITO may offer an enforceable undertaking pursuant to section 259 of the FSA or section 270 of the IFSA. However, it should be noted that BNM may also incorporate similar requirements as part of the licensing conditions of the DITO applicant.

Minimum Paid-Up Capital

RM40,000,000.00 minimum paid-up capital requirement during a DITO’s foundational phase (subject to compliance with other BNM capital requirements).

5) Business Models

Digital players offering risk-sharing protection schemes (such as crowd sharing, mutual protection or peer-to-peer (P2P) protection schemes) which provide protection to its members or participants against specified risks may be included in the licensing of DITOs.

6) Foundational Phase

BNM is exploring a foundational phase for licensed DITOs for a specified number of years from commencement of a DITO’s operations where regulatory flexibilities may be granted. Upon completion of the foundational phase, licensed DITOs will be expected to comply with similar prevailing requirements and will be allowed similar business scope applicable to existing insurance and takaful players.

Please note that:

- The Discussion Paper only sets out the proposed framework for licensing of DITOs; BNM is expected to issue an exposure draft, followed by policy documents on prudential and business conduct requirements for DITOs, later this year.

- Applications for licensing of DITOs will only open upon announcement by BNM.

Contributed by:

Chong Mei Mei (Partner)

(T): 603 – 2632 9887

(E): chongmeimei@rdl.com.my

Priyanka Prabhakaran (Associate)

(T): 603 – 2632 9951

(E): priyanka@rdl.com.my